DIGITAL ASSET ADOPTION: DIGITAL MONIES

Blockchain Coinvestors Letter From London

Vol. 1, No. 4, October 2022

Digital Asset Adoption: Digital Monies

When we digitalized the world’s communications and content with the Internet on its protocol TCP/IP, we failed to get around to commerce – the tools for truly digitalized transactions simply weren’t ready. Now, with the emergence of blockchain technology, the world is moving on to finish the job and the adoption curves are remarkably similar in direction (see above). As we show below, the world is beginning to understand that there are much more efficient and accessible ways to facilitate global commerce than through our existing payment infrastructure which is costly, slow, and hard for many to access. The digitalization of money is critical because quite simply, we all transact, all of the time.

Today’s Payment System: The Problem

In worldwide payments the problem is 6%... in fees that is. According to the World Bank, the average cost for sending money internationally remains stubbornly high at 6%. But of course, this is a simple average, and not all transactions are created equal. For instance, the average cost of a transfer from the US to Nigeria is 1.0%, while from Cameroon to Nigeria charges exceed 10%. Averages also lie because some transfers between, for example, large financial institutions or multinationals, may be in the many hundreds of millions, while retail transactions can be in the handful of dollars. The number 6% is for the average of all transactions. Retail customers (you and I) may find that our fees are a multiple of these averages.

Just as a thought experiment, take a look at how much you would pay to make a bank international remittance from, for example, a bank account in San Francisco to your child on a term abroad in Abadan, Nigeria. The banks would take perhaps $25 in fees on a $100 transfer, and would take a week or so including the need to talk to you in person over the phone. $75 arriving in Abadan before the receiving bank decides whether or not to also levy an inbound wire fee. By the way, it would be similar if your child was in London or Lima.

Now that’s what we call friction!

These statistics remind us that even the most technologically sophisticated part of the global financial system – payments – is far from low cost, fast, and easy.

Why can we communicate at next to no cost in real time, but we can’t transact without massive deadweight loss?

Needless to say, new value propositions are emerging, and the global financial system is in the midst of a transition to digitalized monies and transactions. Traditional financial systems are about to experience a massive transformation and all of the world’s payment infrastructure is about to be upgraded and disrupted.

Legacy System Being Disrupted Today

The global financial system currently consists of many large, highly verticalized financial players, who offer exclusive products and services within walled gardens, for which they can extract sizeable rents. For users this means paying fees to move money in and out of their accounts, into different banks, across networks, across state lines, into new countries. Blockchain technology provides a shared, user-owned base layer that underlies and spans all of these walled gardens, democratizing access to secure financial services, and eroding the network barrier for which these legacy institutions have been able to extract exorbitant fees.

Nowhere is this promise more hopeful than in emerging economies. In fact, as we outline below, developing economies, alongside the digital native generation in high income countries, lead the way in global digital payments adoption.

What’s more, these trends remain robust despite a recent drawdown in prices, as the underlying factors driving adoption are somewhat independent of public token prices

There are four specific use cases that are already migrating towards digital payment approaches in emerging markets. They are:

Remittances

Payments

Access to US Dollars

Economic Opportunity

Below, we dive into some of factors driving these trends. In short, we see the underlying factors driving adoption – in both the developing and developed economies – are sustainable and consistent with our long-term thesis of a shift toward a worldwide digital economy in which each of communications, content, and commerce have been fully digitalized – today at best we have digitalized the first two, with accelerating progress in digitalizing the third.

Global Digital Money Adoption: Emerging Economies Lead the Way

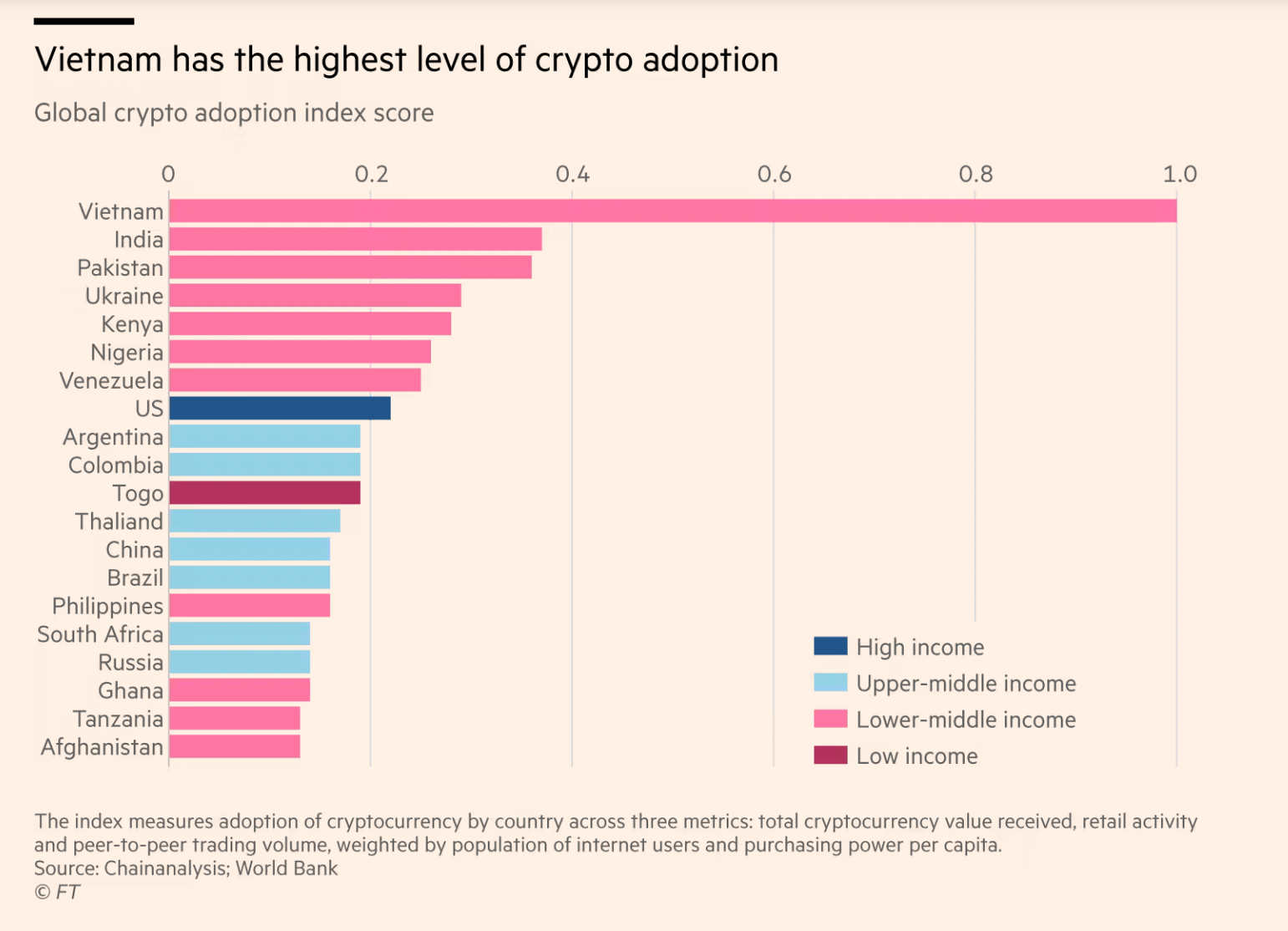

Although crypto adoption has accelerated globally over the past few years, emerging economies are most certainly leading the way. Chainalysis recently ranked Vietnam as the top country for cryptocurrency adoption, with the Asian continent accounting for more than half of all cryptocurrency users globally.

Africa has been equally striking in its embrace of cryptocurrencies. Adoption in Africa grew 1,200% between July 2020 and June 2021, making it the fastest adoption rate in the world (as compared to 800% globally). Africa amassed $106bn worth of cryptocurrencies for the year ending June 2021, driven by peer-to-peer transactions in key growth markets. It is estimated that over ⅓ of Nigerians own, or have transacted with, cryptocurrencies. However, this staggering growth of adoption is not limited to just Africa and Asia. Venezuela, in 2021, broke into the top 10, making it the first Latin American country to do so. As you can see below, there’s a clear adoption skew toward middle income and lower-middle income countries.

But why have individuals in developing economies embraced digital monies faster than those in wealthier nations? While the answer to this question is multifaceted and nuanced, we attempt to lay out a few of the most impactful factors below:

1) Currency Stability

In many developing economies, conventional currencies have long struggled to maintain their purchasing power; double digit inflation has and remains rampant. For instance, the most recent Nigerian inflation exceeded 20%, Pakistan more than 10%, and Venezuela more than 30%. This is a trend that unfortunately has remained consistent throughout recent history; in Inflation in Emerging and Developing Economies, the editors point out that median inflation “was 14 percent in Latin America during the 1980s and 128 percent in Eastern Europe and Central Asia during the first half of the 1990s.” The unfortunate truth is that many citizens of emerging economies have come to expect a significant loss of value in their native currencies and are eager to find alternative stores of value.

2) Archaic Financial and Payment Systems

As noted above, sending money across borders is time-consuming and most importantly, very costly. Thus, it is unsurprising that blockchain powered transactions, with minimal fees and real time settlement and finality, are rapidly growing in popularity where remittances are a major source of income and payment channels remain undeveloped.

3) Limited Access to US Dollars

Approximately 50% of global trade is invoiced in dollars – even if neither counterparty is US-based. In fact, settlement in dollars is required for many essential foreign transactions, including importation of raw materials or foreign services. Additionally, many governments act to severely restrict access to dollars; most Kenyan businesses now have a daily dollar transaction cap for instance and Nigerian banks have limited their customers to spending $20 per month. Hence, it’s not surprising that there is a significant dollar shortage in many emerging economies. Digital transaction infrastructure, such as exchanges and payment channels, which facilitate access to US-dollar stablecoins can significantly alleviate this problem for consumers and enterprises alike.

Digital Money Adoption in Emerging Economies: Practical and Pragmatic Use-Cases

But what are individuals actually using cryptocurrencies and digital monies for in developing countries? We distill a few of the key use-cases below to which the research and data point:

A) Remittances

Remittance inflows from abroad are a major economic asset for developing countries and a crucial backbone of their respective economies. For instance, countries such as Nepal, El Salvador, Haiti, and Lebanon have remittance inflows amounting to over 20% of their annual GDP. It is no surprise that the rate of adoption of cryptocurrencies is closely correlated to the importance of remittance inflows for the economy.

In South Asia, Pakistan, Bangladesh, and India represent remittance markets of over $20bn and blockchain-based payment providers are challenging traditional intermediaries, who as we have noted, traditionally charge exorbitant fees. Some of these payment rails are being built in coordination with government agencies; the Central Bank of the Philippines has approved several crypto exchanges to operate as remittance and transfer companies in the country. Similarly, Sub-Saharan Africa received an estimated $48 billion worth of remittances in 2019, about half of which went to Nigeria, according to a Brookings Institute study.

B) Point of Sale Payments

Many developing countries have also taken steps to accept cryptocurrency as a form of payment for everyday transactions. In Latin America, El Salvador passed legislation to designate Bitcoin as legal tender while in Venezuela, certain cryptocurrencies are commonly accepted as a form of payment, even at major businesses such as the Simón Bolívar International Airport and supermarket chain Bio Mercados.

Likewise, Africa has seen substantial retail payment activity, particularly with regards to smaller everyday payment activity. According to Chainalysis, more than 80% of activity is concentrated in payments of less than $1,000, which is the highest ratio globally.

Finally, Asian retailers are embracing crypto payments, which is unsurprising given the broad adoption already noted. This trend is likely to increase in the near term as a recent Visa survey concluded two-thirds of Southeast Asian want access to crypto for payments.

C) Access to US Dollars

As noted above, US-dollar stablecoins offer a unique ability for consumers and enterprises to get access to coveted dollars, in the context of volatile domestic fiat currencies. Chris Maurice, the CEO of the leading African exchange Yellow Card, noted recently that 80%+ of the activity on the exchange was related to dollar backed stablecoins. Indeed, the most used cryptocurrency on the Yellow Card platform is neither Bitcoin nor Ethereum, but rather USDT, a fully collateralized stablecoin managed by Tether. Through blockchain companies such as Yellow Card, consumers have a simple and compliant method to access and hold dollars.

D) Economic Opportunity

Finally, digital monies do have broader applications than payments. One such sub-sector which has driven dramatic user growth is blockchain-based gaming. Blockchain games represent a new model of gaming, often deemed play-to-earn (P2E), and allow users to retain a part of the economic value they are creating.

In particular, the rise of P2E has driven substantial adoption in Asia; According to data from Axie Infinity, whose publisher Sky Maven is based in Vietnam, at its peak over 40% of its 2.8m monthly active users came from the Philippines alone.

While this may come as a surprise to some, the popularity of P2E games in lower- and middle-income countries makes intuitive sense. In the case of the Philippines, the average Axie user at one point could earn more than the national minimum wage simply by playing the game. However, we see this avenue for adoption as less sticky than the practical payment and currency related avenues noted above.

While not as pragmatic nor uncorrelated to public token prices, play-to-earn has demonstrated its potential and remains promising. Casual games may soon serve to accelerate adoption even further – gaming is a universal, language-agnostic, and broadly accessible inroad to blockchain. Gaming has a history bringing new technology to consumers; many of the first computer products and software programs were games (e.g. pong, snake, solitaire, etc.)

Digital Money Adoption in the Developed World: Digital Natives Leading the Way

Although the list of countries with the highest crypto adoption rates is dominated by the developing world, there are interesting patterns regarding crypto adoption in developed economies. The US has the 5th highest adoption rate and the UK the 17th, numbers that should not be ignored given the massive purchasing power of consumers in these jurisdictions. Moreover, while adoption may be half a step behind, the demographic trends paint an interesting picture.

In short, it’s clear that the digital natives – that is the Millenials and Gen Z’s – are adopting digital assets at a much faster rate than older generations. Finder breaks down cryptocurrency ownership by several demographics, including age, and more than half of Americans who own cryptocurrencies are aged 18-34.

Even more interesting is that this trend appears to hold across the developed economies. In fact, this pattern of ownership is by no means exclusive to the US. In Australia, Singapore, the UK, Germany, Sweden, Canada, Norway, and Ireland digital natives represent a majority of the crypto ownership.

This makes intuitive sense and is a foundational pillar of our thesis at Blockchain Coinvestors. Those under the age of 45 have grown up in the digital age; they already socialize online, shop online, play games online, and now work online. They simply expect assets to be natively digital – and frictionless and accessible.

Furthermore, the data show that the age split in developing economies is fairly consistent across generations. This holds with the analysis above - crypto adoption in these jurisdictions is driven by practical and pragmatic needs. All generations require better payments avenues and access to dollars.

On the other hand, older generations in the developed economies don’t have an immediate need for digital monies – they already have access to cheap payment avenues and stable currencies. Instead, the digital natives are driving the adoption because they see the value in a digitalized economic system.

The View from London: Where We’re Headed

1) Europe and UK Nervously Eyeing the Dollar

On this side of the pond, it’s safe to say that European and British regulators alike are nervously, dare we say jealously, eyeing the rise of dollar backed stablecoins; the demand for dollars has not been restricted to developing economies. Since 2020, dollar backed stablecoins have exploded in use, and represent about $150bn in market value. This, according to The Block, accounts for more than 99% of the total stablecoin market, as hitherto there has been scant market demand for euro or pound denominated stablecoins.

Regulators perhaps showed their cards with the recent of the MiCA bill as mentioned in Letter from London Vol. 2. In a final version now moving to EU approval, regulators seek to cap the maximum amount of non-euro stablecoins (that is US dollar stablecoins) an issuer is permitted to issue within the EU.

Clearly the EU and UK are going to be playing a lot of catch up here. The demand for digital dollars, in the form of stablecoins, seems to have the Europeans worried.

1) Chance to Extend US Monetary Hegemony

The digitalization of dollars represents an attractive avenue for the US to further externalize its financial system and maintain its monetary hegemony. The Federal Reserve recently announced it wouldn’t pursue a CBDC, or central bank digital currency, which would have widely been viewed as a competitor to the privately issued stablecoins such as USDT or USDC. We see this as a prudent move given how quickly the private market has innovated.

We see substantial potential for a public-private partnership in lieu of a Federal Reserve CBDC. For instance, the Fed could move to give Circle, the manager of USDC, a direct account, effectively removing any distinction between USDC and actual dollars.

Regardless, as outlined above, global demand for dollars is intensifying and prudent US regulation may help facilitate another generation of US financial hegemony.

2) The Bear Market Doesn’t Change Adoption Dynamics

Lastly, despite a ‘bear’ market in public token prices, we remain bullish, long-term investors. The adoption dynamics noted above in the developing economies are substantially sticky given their practical use in everyday life. These economies have young, fast growing, and increasingly online populations who have adopted digital monies faster than their counterparts in richer nations. The benefits are significant in these jurisdictions and that has created compelling use cases. Moreover, the digital natives will continue to drive adoption in the developed economies. As noted in Letter from London Vol. 3, the largest institutions are leaning in, largely in an attempt to capture this attractive demographic. BNY Mellon recently announced they will start to custody bitcoin and other digital assets, while Blackrock and Fidelity are offering exposure to Bitcoin and Ethereum. Clearly the largest financial institutions are positioning for the next bull market and positioning as the digital natives move into their heavy earning years. If that was not compelling enough already, as we write this from London, Google has just announced a similar digital money partnership with Coinbase.

As you might expect based on the analysis above, sophisticated investors have continued to invest in front of these tailwinds despite the downturn. Indeed, while prices remain subdued in the context of global macroeconomic uncertainty, if you’re focused on the long term like we are, you should find solace with the underlying factors driving global adoption trends toward a world of ubiquitous digital monies.

Thank you for reading.

Mitch Mechigian, Partner, London

NOTE: We are in the process of our final closing on our currently open fund of funds. Please contact ir@blockchaincoinvestors.com to learn more

ABOUT BLOCKCHAIN COINVESTORS

Launched in 2014, our goal is to provide broad coverage of the emerging unicorns and fastest growth blockchain companies and crypto projects. The strategy is now in its 9th year and has to date invested in more than 40 pure play blockchain venture funds in the Americas, Asia and Europe; and in a combined portfolio of 400+ blockchain and crypto projects including approximately 60% of all blockchain unicorns. Our funds rank in the top decile amongst all funds in their respective categories on both Pitchbook and Preqin. Headquartered in San Francisco with a presence in Grand Cayman, London, New York, Zug and Zurich, the alternative investment management firm was co-founded by Alison Davis and Matthew Le Merle.

FUND PERFORMANCE

Blockchain Coinvestors Fund III (Fund of Funds) was created to provide diverse coverage of the best blockchain pure play venture funds in the Americas, Asia, and Europe. Blockchain Coinvestors Funds I and II have already experienced significant appreciation. Fund I Net TVPI is 4.82x with an IRR of 67%. Fund II shows equally impressive early results with Net TVPI of 1.42x and an IRR of 42%. Almost all of our fund investments are performing as top quartile against the Cambridge Associates Venture Benchmark.

BLOCKCHAIN COINVESTORS FUNDS

Blockchain Coinvestors’ goals are to provide broad coverage of the emerging unicorns and fastest growth blockchain companies and to capture superior returns from investing in the leading blockchain venture partnerships. Our funds are open to investors that meet the Qualified Client definition with a minimum subscription level of $250,000 at the discretion of the Manager.

Blockchain Coinvestors Fund III (Fund of Funds) was created to provide diverse coverage of the best blockchain pure play venture funds in the Americas, Asia, and Europe. Blockchain Coinvestors Funds I and II have already experienced significant appreciation. Fund I Net TVPI is 4.82x with an IRR of 67%. Fund II shows equally impressive early results with Net TVPI of 1.42x and an IRR of 42%. Almost all of our fund investments are performing as top quartile against the Cambridge Associates Venture Benchmark.

Blockchain Coinvestors Fund IV (Early Stage Token) provides direct access to promising private stage token projects accessing our relationships with many of the world’s leading blockchain investors. We leverage asymmetrical information from our 40+ VC Funds to pick the most attractive opportunities. This is a continuation of the direct token investing strategy of the Fund Manager that has included private stage investments in Acala, Filecoin, NEAR, Polkadot, Structure, and others.

Blockchain Coinvestors VI (Mid Stage Growth) provides direct exposure to the emerging category leaders in the blockchain and crypto ecosystem. The fund leverages our unique sustainable competitive advantage (USCA) in blockchain, web3, and fintech to create a concentrated portfolio of between 20 and 30 investments with attractive return profiles and visible paths to liquidity. The fund assesses the more than 400 blockchain and crypto projects in which we are direct and indirect investors and employs a robust investment framework to select investment opportunities into the leading mid stage growth rounds - typically Series B, C and D. This is a continuation of the mid stage investing strategy of the Fund Manager that has included investments in Bitwise, Brex, InfiniteWorld, Securitize, Uphold, Wyre, and others.

Please visit the Blockchain Coinvestors website to learn more about our offerings. You can also reach our Investor Relations team directly at ir@blockchaincoinvestors.com.

BLOCKCHAIN COINVESTORS SWISS

We are excited to announce that Blockchain Coinvestors Funds are now available through Swiss certificates for those of our non-US investors who prefer this approach. The underlying fund is the same, however, our Zurich based team at Blockchain Coinvestors Swiss, who will introduce in future weeks, can provide detailed information regarding this investment option. Email us at mlemerle@blockchaincoinvestors.com to learn more.

BLOCKCHAIN COINVESTORS ANGELLIST SYNDICATE

Continuing the theme of the democratization of investing, we have a rapidly growing Blockchain Coinvestors syndicate on AngelList providing access to selected coinvestments. Please join us and our partner Lou Kerner on AngelList.

Click here to receive the insightful weekly crypto newsletter and webinar invitations from our Blockchain Coinvestors partner Lou Kerner.

FinAccelerate is an intense accelerator program empowered by one of the world's leading and largest law firms, Jones Day. The program covers the fundamental areas of law relevant to innovative fintech companies and enables selected fintech businesses to access leading investors, corporations, financial institutions, and potential JV partners to accelerate their business.

Over the course of 3 days, applicants have the opportunity to engage with a strong ecosystem of world-leading advisors, investors, and partners to the program, like Matthew Le Merle of Blockchain Coinvestors, Chris Larsen from Ripple Labs, and Andrew Siegel of Galaxy Digital.

REGISTER NOW FOR UPCOMING WEBINARS AND CALLS

Our investment team hosts regular webinars and calls to help educate our community about the Fifth Era, fintech, blockchain and crypto. We discuss important trends, tailwinds and investment themes including what we have learned and how we are using our knowledge to inform our own investment thesis and actions. Below is a list of upcoming webinars for which you can register by clicking the links:

2023 Blockchain Predictions

- November 7th, 7:00am PT

- November 7th, 12:00pm PT

Options for Investing in Blockchain & Crypto

- November 14th, 7:00am PT

- November 14th, 12:00pm PT

Meet the Blockchain Unicorns - Year-End 2022

- December 5th, 7:00am PT

- December 5th, 12:00pm PT

Recordings of past webinars and calls can be found at www.blockchaincoinvestors.com/webinars.

RECENT PRESS

CoinTelegraph: The impact of crypto on the Russian sanctions

Ageless and Timeless: Conversation on how blockchain and crypto technologies will impact the future

CoinDesk TV: Interview on unicorns and predictions for 2022

Nasdaq Trade Talks: Discussion on the blockchain unicorn universe research and how to gain exposure

CoinDesk: Our predictions on blockchain unicorns in 2021

Ashurst: On the ESG Podcast, a discussion of the internet, fintech, blockchain, and individual revolution

Business Insider: Discussing how right now in blockchain is similar to the internet boom of the '90s in terms of growth and innovation

NBC San Francisco: An interview on what are NFTs

US News & World Report: What to know about Bitcoin ETFs

Crypto Unstacked: Podcast on the Fifth Era and the evolution of digital assets

Business Insider: Which digital asset to hold right now - Bitcoin or Ethereum

Inc Magazine: An explanation of NFTs

Pensions & Investments: How institutional investors are getting closer to blockchain and crypto investments

On the Brink with Castle Island: An overview of technology trends and the cryptoasset markets